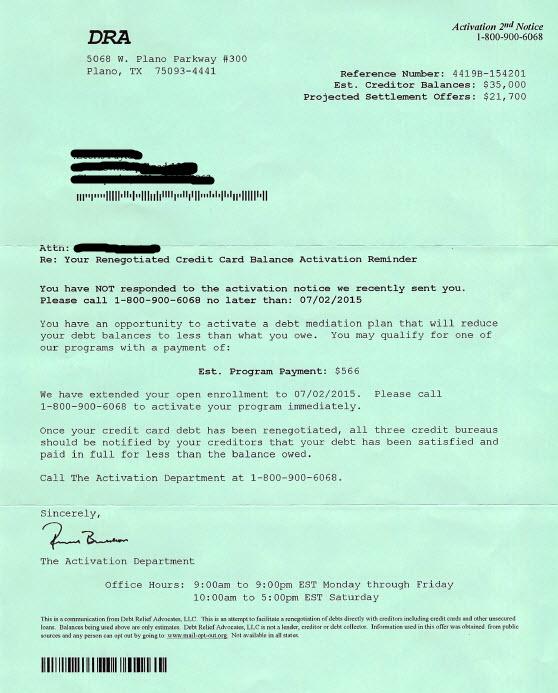

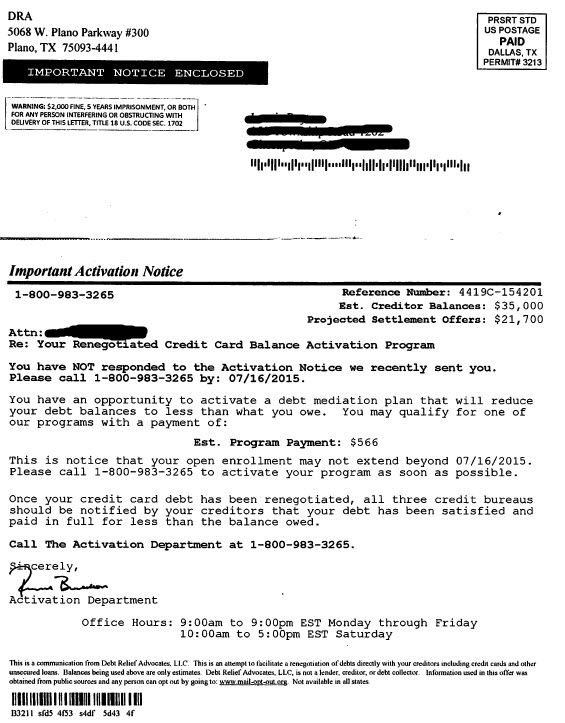

Warning – if you have received a letter from DRA (Debt Relief Advocates LLC), it may be a part of the latest scam that preys on seniors suggesting to them that they owe debts that DRA can settle for less. In most cases – there isn’t even a debt owed at all.

Warning – if you have received a letter from DRA (Debt Relief Advocates LLC), it may be a part of the latest scam that preys on seniors suggesting to them that they owe debts that DRA can settle for less. In most cases – there isn’t even a debt owed at all.

An Ohio case was just settled against them and they are probably sending out these letters to other states as well. The Ohio lawsuit claimed that the consumer was sent an offer to settle a debt by DRA. But what’s interesting is that the allegation made by the consumer states that they did not owe this debt DRA claimed that they did owe.

DRA violated R.C. §1345.02 and committed an unfair or deceptive act or practice in connection with a consumer transaction because DRA offered debt mediation services when DRA knew that Plaintiff did not owe an debt obligation and Plaintiff had an inability to receive a substantial benefit from DRA’s services.

According to this complaint, the consumer was mailed letters offering to renegotiate a non-existent debt along with many phone calls to her home Continue Reading ›