How can I stop an Order of Replevin? If someone has received an Order of Replevin, (a legal procedure used to recover property) it probably is for property used as collateral on a loan or being purchased through a loan agreement by that person. The lien holder desires to repossess the property (car, furniture, mobile home, shed, trailer, equipment, etc) and has filed a lawsuit and received an Order of Replevin against the debtor because the debtor refuses to surrender the property voluntarily.

How can I stop an Order of Replevin? If someone has received an Order of Replevin, (a legal procedure used to recover property) it probably is for property used as collateral on a loan or being purchased through a loan agreement by that person. The lien holder desires to repossess the property (car, furniture, mobile home, shed, trailer, equipment, etc) and has filed a lawsuit and received an Order of Replevin against the debtor because the debtor refuses to surrender the property voluntarily.

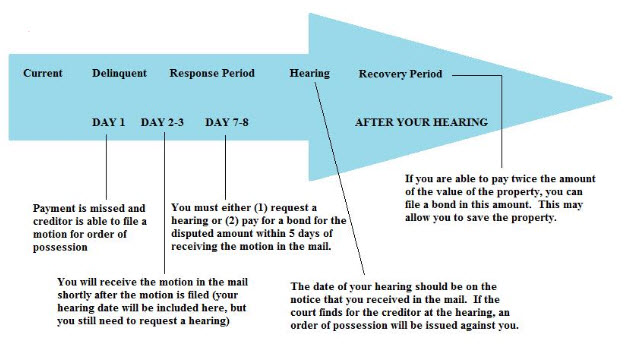

The best way to stop an Order of Replevin is to not let it get to the stage of the Order being issued. You need to address things once the lawsuit has been filed against you by the person/company seeking the Replevin – stopping an order from being issued in the first place. This lawsuit is filed and called a “Writ of Replevin”. When you receive notice of this lawsuit, respond! If you fail to do anything, an Order of Replevin will be issued to the person/company seeking it. You should have received a Replevin Summons (Notice to Appear in Court) and been given 20 days to respond to the lawsuit to fight it. If you fail to respond, the person/company will file for a default judgment. After the default (or final hearing), the judge will grant the final judgment (Order of Replevin).

Speak with an attorney. You can stop a Writ of Replevin by fighting the lawsuit itself or, if the debt is legitimate and you are behind without the ability to catch up, you can file a Chapter 7 or Chapter 13 Bankruptcy case. The bankruptcy case will stop the Replevin action in it’s tracks. Depending upon which type of bankruptcy you file, you will either retain and pay under new terms for the property or you will surrender the property at a later date, established through the bankruptcy court process.